BNPL is not just a payment option. It reflects a shift in consumer behavior, where instant purchasing aligns with structured financial control. This is why BNPL app development has become a priority for businesses that want to make high-value purchases more accessible to customers.

Recent stats highlight just how fast its market is moving:

- The global BNPL market is expected to grow from $54.56 billion in 2026 to $286.02 billion by 2034. (Source: Fortune Business Insights )

- BNPL users are projected to rise from 380 million in 2024 to 670 million by 2027. (Source: Juniper Research)

It leaves no doubt why the BNPL platforms are attracting more investors and founders. However, if you’re also planning to build a BNPL app this year or next, you should know that you’re stepping into a market where BNPL solutions are no longer limited to traditional eCommerce checkouts.

The entry of AI commerce, agentic commerce, and generative commerce to BNPL has made it shift beyond high-ticket purchases and has become a part of routine transactions.

Hence, if you want to create a BNPL app today you cannot build for a market that existed a year before to now. The BNPL platform development approaches that worked then cannot help you sustain the long game anymore.

You now need to engineer a BNPL platform that’s not only scalable, highly regulated, and compliant, but also built for AI-powered shopping experiences, where AI agents are assisting customers throughout their journey from product discovery to purchase.

While this opens a massive opportunity, it also presents a fresh set of challenges around development costs, compliance, credit risk, security, and AI integration.

To guide you on how to build a BNPL app that meets today’s market demands, I have prepared an extensive BNPL app development guide with the help of my in-house fintech app development experts and research from HBR and PWC papers. It covers essentials like types of BNPL business models, how top BNPL apps have repositioned to meet the agentic demands, key features to add in a BNPL app, the development process, the cost estimate, and so on.

What is BNPL and How Does it Work?

BNPL stands for Buy Now, Pay Later, and it gives consumers the freedom to make small to big purchases instantly and pay them in installments.

What is BNPL?

BNPL is a short-term debt financing solution that allows consumers to purchase products & services instantly and pay in installments, usually without interest.

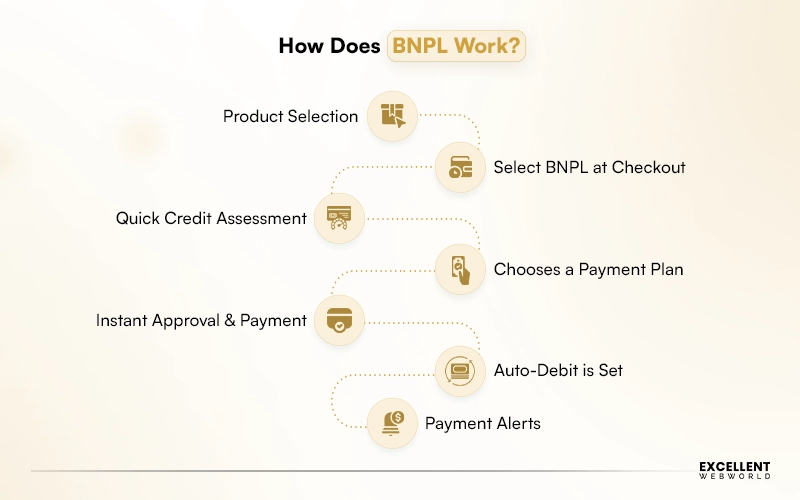

How Does BNPL Work?

The Buy Now, Pay Later model gives consumers the power to purchase products anytime and merchants the ability to receive full payments. Here is how BNPL apps work generally.

- Product Selection: Customers browse products on an eCommerce platform or in-store and add the required products to their cart.

- Select BNPL at Checkout: During checkout, a customer chooses BNPL as their preferred payment option when purchasing a product or service.

- Quick Credit Assessment: The BNPL app conducts a real-time credit evaluation using credit check & customer shopping behavior, without impacting their credit score.

- Chooses a Payment Plan: The app then showcases different payment plans, such as, Pay-in-4(Splits), a deferred payment model ( pay later), and installment-based BNPL(long-term).

- Instant Approval and Payment: The consumer reviews and agrees to the payment plan, and the purchase is confirmed. The BNPL provider pays the full product amount to the merchant within 24-48 hours, without affecting their cash flow.

- Auto-Debit is Set: All payments are automatically debited from the customer’s bank account or card according to the schedule.

- Payment Alerts: The platform sends reminders and alerts for upcoming or missed payments, along with applicable charges as per policy.

BNPL vs Traditional Credit Systems

BNPL provides short-term, interest-free installment payments with minimal friction for certain purchases. In contrast, traditional credit (credit cards) provides revolving credit for broader use, built-in rewards, and strong consumer protections, but involves longer approval cycles, fixed limits, and interest-based payments.

Let’s compare BNPL vs traditional credit systems in detail.

| Aspect | BNPL | Traditional Credit Systems |

|---|---|---|

| Approval Speed | Instant(Seconds) | Days to Weeks |

| Credit Check | Soft or Minimal Check | Hard Credit Check |

| Costs & Interests | Zero or minimal if paid on time | High-interest rates |

| Accessibility | High (even for users without a credit history) | Limited to users with a credit history |

| Protection | Less Protection | High Consumer Protection |

| Repayment Period | Fixed short-term installments(4-6 Weeks) | Revolving Credit or Long-term EMI |

| Impact on Credit Score | Minimal to None | Affects Credit Score |

| Use Case | Specific Purchases | Broad Financial Needs |

What are the Types of BNPL Business Models

The BNPL platform is usually categorized into 4 models: merchant-funded, consumer-funded, hybrid (merchant+consumer), and, lastly, BNPL-as-a-service (BaaS). These are divided based on who bears the fees, how revenue is generated, and who serves as the primary stakeholder. Let’s look at them in detail.

Merchant-Funded Model

In the merchant-funded BNPL model, the merchant pays a fee to the BNPL platform for each transaction, typically 2-8%. The main aim is to provide consumers with interest-free payments on their end. By reducing upfront payment costs, the merchant drives higher conversions, increases order value, and reduces card abandonment.

Consumer-Funded Model (Interest-Based)

The consumer-funded BNPL model is a type of short-term financing in which consumers pay fees to the BNPL provider through interest or late fees. This model works well for large purchases with longer repayment periods. It increases the profit margins of BNPL providers while offering consumers greater flexibility than traditional credit.

Hybrid Model (Merchant + Consumer Fees)

The hybrid model divides the fees between the merchant and the consumer. A merchant pays fees for each transaction, while the consumer pays fees for interest or extended plans. The balanced approach results in a profitable and scalable revenue model for BNPL providers that want to target low and high-ticket sales.

BNPL-as-a-Service (BaaS)

Providers allow banks, fintechs, and retailers to launch a white-label BNPL solution on existing infrastructure, which covers the credit engine, compliance, and payment processing layer. Businesses can launch a BNPL platform without building from scratch through APIs and SDKs.

BaaS remains one of the leading BNPL models in 2026. It is one of the most natural ways to expose BNPL to AI agents and embedded checkout experiences, helping businesses increase conversion rates and order values. The same APIs that serve merchants can now serve AI-powered shopping agents, creating new opportunities for embedded finance.

Top BNPL Apps and How They’ve Repositioned To Meet Agentic AI Demands

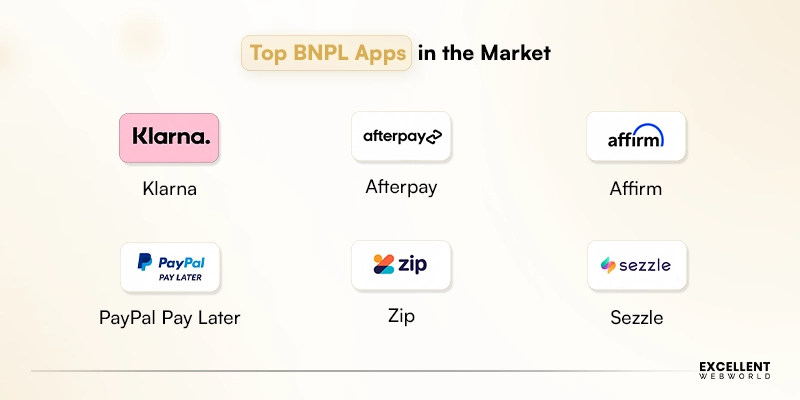

The top BNPL apps, such as Klarna, Afterpay, PayPal Pay Later, Affirm, Zip, and Sezzle, are dominating the market. These apps offer flexible installment payments tailored to the consumer’s spending habits.

The familiar players still lead, but the important 2026 story is that they have become distribution nodes inside AI assistant, wallet, and platform ecosystems rather than standalone destinations.

Klarna

Klarna is a Sweden-based BNPL provider with a presence in more than 45 countries. It offers Pay-in-4, pay-in-30-days, and longer-term financing.

Beyond its own platform, Klarna has slowly integrated into AI-powered shopping experiences, along with Google’s AI shopping ecosystem and agentic commerce initiated through Stripe, which showcase the growing adoption of BNPL and AI-driven commerce.

This denotes that Klarna doesn’t just act as a traditional BNPL provider but also is responsible for emerging AI-assisted purchasing journeys across multiple digital touchpoints.

Afterpay

Founded in Australia, Afterpay enables customers to split purchases into four equal, interest-free payments. It integrates instantly with the checkout and allows users to manage expenses, along with supporting higher conversion rates. It is adopted by top brands across the fashion, beauty, and lifestyle categories, such as Uber, Airbnb, IKEA, Ticketmaster, and more.

Affirm

Affirm is one of the leading BNPL providers in the US, known for installment-based payments with no late fees, penalties, or hidden costs. It has strengthened its position across everyday transactions and high-value purchases, with Amazon and Walmart both integrating it into their retail ecosystems. Affirm is among the first BNPL providers to adopt agentic commerce via Google and Stripe, built to be selected by AI agents for autonomous purchases rather than human shoppers.

PayPal Pay Later

Built on PayPal’s existing merchant ecosystem, it allows consumers to divide their purchases into manageable installments. It provides two pay-later options: Pay-in-4 and monthly, to provide a fast checkout experience to customers. Its deep integration across millions of online stores gives it a distribution advantage that standalone BNPL providers cannot match.— and a strong base for embedded and agent-led checkout.

Zip

Founded in Australia, Zip uses a reusable credit line to split purchases over time with zero interest. The platform offers a virtual card for in-store and online purchases across various retail categories.

Sezzle

Sezzle is a popular US-based BNPL platform that lets users split their purchases into 4 interest-free payments over 6 weeks, with minimal credit requirements. The platform features encourage responsible spending and enhance user engagement over time.

BNPL in the Age of AI Agents

BNPL is moving well beyond the traditional checkout experience. Due to the increasing adoption of AI-powered shopping experiences and agentic commerce, consumers can now discover relevant products, compare options, and make purchases through AI-based experiences. Hence, BNPL is increasingly added as a source of payments in AI-powered marketplaces and super apps, which leads to stronger opportunities for fintech providers, merchants, and retailers.

What is Changing?

AI is not just limited to product search and recommendations. Modern AI agents do all the work, right from the product search to the last transaction on the user’s behalf. To adopt this quickly, payment networks, technology providers, and BNPL platforms are building infrastructure that enables secure and compliant AI-driven transactions.

Several industry developments are accelerating this transformation:

- Network Frameworks: Visa and Mastercard are releasing standardized frameworks for AI-driven transactions, which allows autonomous AI agents to complete all the purchases on-the-go on the user’s behalf.

- BNPL inside AI Assistants: Tech giant Google has made a collaboration with Affirm and Klarna to ensure BNPL is available under AI shopping experiences. Stripe, a leading financial services platform, has also expanded agentic commerce support through Affirm and Klarna. Hence, BNPL is increasingly becoming available within AI assistants, digital wallets, and shopping experiences instead of just merchant checkout pages.

- BNPL Inside Agent Checkout: BNPL is not just a payment option for customers at checkout. It is now being integrated into AI-agent purchase flows, which means more financing options remain available when AI agents assist users throughout the purchase.

In an agent-based purchase, your BNPL platform is not competing as an option that a consumer chooses during manual checkout. Instead, it is competing to be a financial option an agent considers to explore, analyze, and recommend.

This shift showcases the real value of well-documented APIs, machine-readable offer data, structured offer data, and consent mechanisms built specially for AI-driven transactions rather than traditional human-only checkout experiences.

AI-Native Payments: The New Technical Surface

Agent-initiated transactions have several kinds of security and trust issues that traditional checkout methods rarely face. Therefore, when AI agents get involved in commerce, BNPL platforms should include additional layers of verification, consent, and authorization. AI-native payments help address these challenges, and there are several components that should be present in it.

- Agent Verification: Validating through cryptographic or token-based proof that the AI agent is authorized to act as a human before beginning any transaction.

- Real-Time Content Flows: AI agent captures user approval for purchases, spending limits, and repayment plans at the point of transaction.

- Machine-Readable Offers: Showcasing BNPL terms (plan options, fees, schedules) in a structured form that AI systems can interpret and compare.

- Programmable, Behavior-based Offers: Generating and pricing a personalized BNPL offer according to a user’s behavior, transaction history, and basket value, then returning it via APIs to AI agents in real time.

What to do about it? An AI-native BNPL platform in 2026 should present its credit decisioning and offer engineers via an API-first architecture that supports merchants, AI-powered shopping agents, and embedded commerce experiences. Businesses should consider agent verification and consent management as the main components of their authentication strategy and align with emerging network frameworks from Visa and Mastercard rather than assuming a human-only checkout.

Recommended Key Features to Add to a BNPL App

A modern solution combines the essential BNPL app features with the most advanced ones to deliver a seamless payment experience and drive adoption. From user registration, repayment management, and compliance to AI-driven intelligence and emerging AI-powered commerce experiences, a competitive BNPL app in 2026 requires a comprehensive set of features. Here is what you should scope.

Core Features of BNPL App

Here are some essential features for building a reliable and intuitive BNPL App.

- User Registration & Authentication: Allow users to sign up via email, phone number, or social login for secure identity creation and a seamless onboarding experience.

- Payment Scheduling & Auto-Debit: The BNPL platform splits payments into equal installments, debits payments on specified dates, and allows users to reschedule payments to make manual payments when needed.

- Merchant Integration & Payment Gateway: BNPL platform integrates well with the merchant platforms and payment gateways to ensure a smooth and uninterrupted experience online and offline.

- Transaction History: Users can view all their purchases, pending installments, completed payments, refunds, and more by downloading statements for record-keeping.

- Push Notifications & Payment Reminders: The BNPL app should send push notifications for upcoming due dates, new offers, payment confirmations, and account updates, which results in reduced missed payments and better user engagement and retention.

- Soft Credit Check: The app should integrate with popular credit bureaus such as Experian, Equifax, and TransUnion for risk checks without affecting credit scores.

Advanced AI-Driven Features to Add to BNPL App

Beyond the basics, the following fintech lending app features set a competitive BNPL platform apart and align with the top tech trends shaping the industry in 2026.

- AI-Powered Real-Time Risk Assessment & Fraud Detection: AI-powered models help BNPL platforms make smarter lending decisions by analyzing transaction patterns, spending behavior, repayment history, and suspicious activities in real time. The right BNPL app development partner combines AI with robust compliance and security frameworks to improve accuracy, reduce fraud risks, and enhance customer experience.

- AI-based Analytics & Reporting: AI-powered analytics tools help merchants and admins track spending behavior, repayment trends, default risks, performance metrics, and user engagement through a centralized dashboard.

- AI-driven Credit Scoring: An advanced BNPL platform should use AI models and machine learning to evaluate user creditworthiness by looking at behavioral, transactional, and alternative data beyond traditional credit bureaus.

- Personalized Credit Limits: The system should adjust user limits based on behavior, repayment history, and engagement to deliver a tailored experience. Real-world implementations, such as this fashion eCommerce app case study, showcase the impact of personalization on user retention and conversions.

- Virtual Cards (One-time-use cards): The app generates a virtual card for one-time payments to reduce fraud and ensure secure transactions.

- Multi-currency Support: An advanced BNPL app supports multiple currencies and exchange rates to make it available to global users and merchants.

- Loyalty Programs and Rewards: There should be built-in reward systems, such as cashback, reward points, or exclusive offers, that drive repeat purchases and user engagement.

- Conversational AI Support: Using AI-based chatbots, the app not only resolves queries in real time but also offers personalized assistance and payment reminders.

- AI Visual Search: Users can search and shop for products by uploading images or scanning items directly, and the platform instantly connects them to the BNPL payment option.

We offer AI visual search as a ready-to-deploy product that businesses can integrate into their BNPL platform to enhance product discovery, improve user experience, and increase conversion rate.

Agent-Readiness Features

As AI-powered eCommerce continues to grow, BNPL platforms should start adopting features that ensure smooth interactions with AI assistants, shopping agents, and embedded eCommerce experiences. The following features allow businesses to build BNPL platforms that align with the purchase behaviors and outperform outdated architectures.

- Agent-Consumable Layer: Credit decisioning and financing offer engines are exposed via well-documented APIs. These can be accessed by merchants, embedded commerce platforms, and AI-powered shopping agents.

- Agent Verification and Scoped Consent: First-class verification and consent flows are implemented to confirm an AI agent’s authority to act on a user’s behalf. Real-time, auditable approval is captured during the transaction rather than solely during user onboarding.

- Machine-readable Financing Offers: Structured BNPL plans, fees, payment schedules are presented in a structured format that AI systems can parse, compare and present to users; not just rendered UI copy for human readers.

Compliance & KYC Features in BNPL App Development (Region-Specific)

Regulations vary by region, which is why compliance is an essential part of BNPL app development. The table below highlights the key regulatory bodies and the compliance requirements across various regions worldwide.

| Region | Regulatory Body | Key Requirements |

|---|---|---|

| USA | CFPB+ State Regulators | Truth in Lending Act (TILA), CFPB oversight, consumer protection laws, credit reporting rules, PCI-DSS compliance |

| Europe | European Commission EBA (supporting authority) | GDPR compliance, EU Consumer Credit Directive 2023, data protection, transparent lending and disclosure norms |

| Australia | ASIC | NCCP Act compliance, aAustralian Credit Licence (ACL), responsible lending obligations, and AFCA membership (where applicable) |

| Signapore | MAS | KYC and AML compliance, MAS oversight and BNPL industry code of conduct, Consumer data protection, increasing regulatory oversight |

| GCC(UAE, Saudi Arabia) | CBUAE (Central Bank of UAE) SAMA (Saudi Central Bank) | Central Bank Licensing required, KYC and AML compliance, sharia-compliant structures, consumer protection rules, credit limits, transparent fee disclosures |

BNPL App Architecture & Tech Stack

A well-built BNPL app is a combination of a layered architecture and a tech stack, with components that support each other to enable real-time credit decisions, secure payments, and a seamless user experience. Understanding the architecture and tech stack speeds up the BNPL app development.

BNPL App Architecture Overview

A BNPL app architecture comprises five different layers with each designed to perform specific functions. From a user-facing frontend to backend credit logic, database management, and third-party integrations, each layer works in sync to help with real-time decisions, secure transactions, data storage, and platform scalability.

- User App (Frontend): The frontend delivers an intuitive and seamless interface that helps users with registration, browsing, checkout, and payment tracking across mobile and web platforms.

- Merchant System Integration: This layer connects the BNPL platform to the merchant ecosystems, AI agents, embedded commerce environments via APIs and SDS, which facilitates real-time financing, payment processing, and transaction flow online and in-store.

- Backend(Core Logic & Credit Engine): The main part of the platform handles business logic, user authentication, and credit decision making to deliver accurate, real-time approval outcomes.

- Database Layer: A robust database layer stores user data, transaction records, repayment schedules, and compliance data for instant retrieval and processing. To achieve this, it is essential to consider a cloud storage solution that manages both structured and unstructured data in line with regional compliance requirements.

- Third-Party Services: External services support payment processing, identity verification, and credit scoring via secure API integrations.

Editor’s Note: Modern BNPL platforms are built on microservices and API-first architecture, as it allows BNPL services to scale far better than traditional merchant checkout experiences. The API-first core supports AI-powered shopping agents, digital wallets, and embedded commerce platforms to consume your BNPL product directly. As agentic commerce grows in scale and capability, an API-first architecture is becoming non-negotiable to strengthen BNPL capabilities across emerging purchasing channels.

Key Components of the BNPL System

Here are some key components of the BNPL system that define how the platform manages credit, assesses risk, ensures data encryption, and supports user interactions for a seamless payment experience.

- Credit Decision Engine: The main component of the BNPL platform that analyzes user eligibility in real-time by checking credit bureau data, transaction history, and behavioral signals. It approves or declines the purchases to maintain the risk control and lending accuracy.

- Real-time Risk & Fraud Assessment: ML models analyze device usage, transactional velocity, and behavioral patterns. As of 2026, these models even detect agent-impersonation and anomalous agent activity to prevent fraud detection.

- Data Encryption & Privacy Layer: This layer protects sensitive user and transaction data through end-to-end encryption and tokenization. The platform integrates cloud security to comply with regional data privacy regulations and build long-term user trust.

- User Management System: The system handles the entire lifecycle, including user registration, authentication, and all account activities. It manages the lifecycle of users, merchants, and admin profiles, along with scoped agent-consent records as a distinct data entity to ensure secure access control, authorization, personalization, and smooth operations.

- Payment Processing Engine: Engine handles every transaction from start to finish: transaction execution, installment splitting, auto-debit scheduling, retry mechanisms, and refund processing across multiple currencies. Built for accuracy and speed, it ensures every financial operation is seamless and error-free.

- Notification System: The notification system sends real-time alerts for payments, transaction confirmations, and updates via email and SMS. It helps improve user engagement and reduces missed payments through timely communication.

In essence: A robust BNPL system is a combination of credit intelligence, risk control, secure data handling, and smooth payment processing.

Tech Stack for BNPL App Development

Here is a commonly used tech stack for BNPL app development in 2026, designed to support scalability, security, and seamless integrations.

| Layers | Technology |

| Frontend | React Native/ Flutter |

| Backend | Node.js/ Python (Django / FastAPI) |

| Database | PostgreSQL/ MongoDB |

| Cloud | AWS/ Azure/ GCP |

| Integrations | Stripe KYC APIs, Credit Bureau APIs, agent/network frameworks |

| Security | OAuth 2.0, SSL/TLS, AES-256 Encryption, agent verification / consent tokens |

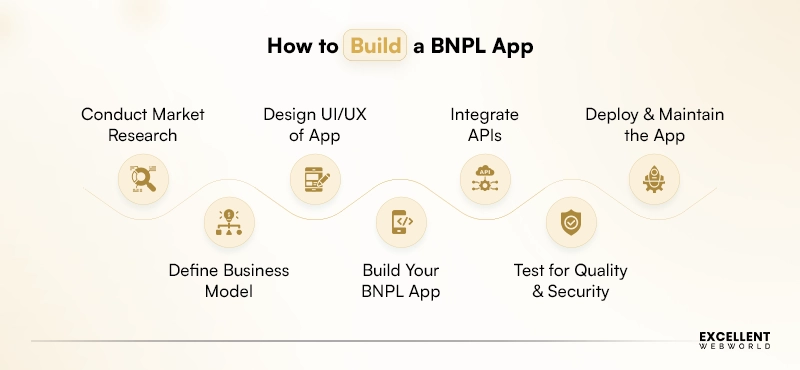

How to Build a BNPL App?

The core mobile app development process is broadly the same; however, now BNPL platform comes with some additional layers: real-time credit decisioning, multi-region compliance, secure financial integrations, and now agent-readiness.

When going through “how to build a BNPL app” guides, they describe the same seven steps: research, define the model, design, build, integrate, test, and launch. That structure is correct. The thing that’s changed is who executes each step and how long it takes. Although, AI has captured a lot of part of work, but not all of it. Here, it’s essential to understand which part of the BNPL platform ships on time and which gets closed by the regulator in six months.

Here’s the honest step-by-step breakdown of the complete fintech app development lifecycle.

1. Research Now Takes a Weekend, Not a Quarter

Extracting how leading BNPL apps like Klarna, Affirm, Tabby, and Tamara actually work, estimating total revenue opportunity, fetching thousands of app store reviews for true consumer complaints, comparing mobile app development technologies, and understanding regulatory compliance; all of this used to consume significant analyst time. Now, it can be completed in a few days using Claude or ChatGPT.

The only limitation is that these tools cannot determine what you are legally allowed to architect.

Whether you need a financing license or must operate under a licensed lender, and what changes when running a BNPL platform under SAMA, CBUAE, or RBI; these decisions carry significant legal consequences and require the guidance of a fintech lawyer, not an AI assistant.

If you do not want to invest your precious time in all this research, you can hire an AI-native software engineering team with deep fintech expertise. They help you make the right decisions based on expert consultation.

2. Analyzing and Picking the Business Model is Still a Human Decision

AI will happily model unit economics with remarkable speed and accuracy. A well-prompted model can build a spreadsheet in minutes covering forecast default scenarios, different revenue streams, late fees, interest scenarios, default curves, cohort projections, customer acquisition costs, and repayment behavior far more efficiently than before.

AI can provide necessary insights and recommendations. However, an AI model cannot help you choose your risk appetite, funding structure, and what you are willing to trade-off to secure a big merchant. Those are CFO and founder decisions, which require commercial judgment, industry expertise, and knowledge of business objectives that no AI tool can replicate.

3. Design Got Faster, but the Critical Screens Still Need Human Expertise

A clickable prototype before signing a contract is the new normal. Tools such as Figma AI, v0, and Claude can produce wireframes, user flows, and a clean first UI within a span of hours instead of weeks.

The challenge here is that a BNPL checkout is not just a landing page. The platform runs in a regulated environment where user trust, transparency, and compliance affect adoption. The most essential screens are the ones that AI does not generate well, which includes mandatory fee disclosures, repayment terms, declined payment paths, partial refunds, disputes, and hardship assistance.

These are the screens where trust and conversion rate matter more than the hero section. They also carry compliance obligations that a generated template will not cover. That is where experienced product designers become essential to craft user journeys that build trust, support compliance, and improve conversion rates.

4. You Can Scaffold the App in a Day. The Financial Logic Is a Different Story

This is where AI hype is both most and least true. Tools such as Cursor, Claude Code, and GitHub Copilot can set up the structure of an app, write CRUD operations, build user interfaces, and connect necessary integrations at a fraction of the time required previously. The routine 70% of the codebase has genuinely been commoditized.

The remaining 30% determines everything. Fintech systems demand absolute accuracy when it comes to building ledgers, payment processing workflows, settlement mechanisms, and credit decisioning engines. Even minor errors can result in reconciliation issues, compliance risks, financial losses, and customer complaints. That’s where senior fintech engineers come into the picture, and they are not a prompt away.

As BNPL platforms continue to evolve, businesses now also utilize Agentic AI development services to build autonomous systems that improve fraud detection, automate credit decisioning, and streamline customer support along with maintaining regulatory compliance.

To achieve the best results, businesses should consider partnering with a team that offers deep fintech expertise. They will follow an agile development process to build, test, and iterate continuously to develop a BNPL app that delivers scalability, performance, and security.

5. API and Third-Party Integrations

AI helps you write integration code against a documented API very easily. However, it falls short when it comes to securing partnerships for credit-bureau access, sponsor banking relationships, local payment rails (KNET, Mada, and others), and trusted KYC/AML vendors. This is because API partnerships involve commercial and legal agreements negotiated by people.

Every integration comes with its own set of operational nuances and undocumented edge cases that rarely appear in documentation. The gap between documentation and real-world implementation can involve significant engineering effort and cost. Hence, partnering with experienced fintech engineers is often the best approach.

6. Testing Got an Assist, but Audits Still Require Human Validation

AI can generate unit tests, integration tests, and accelerate regression testing to flag code-level vulnerabilities quickly, which helps save significant testing time.

However, PCI-DSS scoping, independent penetration testing, AML transaction monitoring validation, and audit readiness require human expertise. No AI tool gets you through a payments compliance review. By partnering with the right fintech app development company, they will look after automated testing as well as third-party compliance obligations. Hence, you can launch your platform with confidence.

7. Deploy Your BNPL App and Maintain It

AI can streamline the deployment activities, such as CI/CD pipelines, infrastructure-as-code, monitoring, and log triage, which enables tram to launch BNPL platforms efficiently.

However, deployment is just the initial thing. Running a live BNPL app includes maintaining merchant uptime, settlement windows, incident response, and regulatory reporting, and adopting compliances such as ZATCA, PDPL, and GCC-specific BNPL regulations. This ongoing cost is the one founders consistently forget to budget for.

The Honest Takeaway: The conversation is not “use AI or hire a team.” That framing is outdated. AI has already removed the commodity layer, which comprises research, app structure, and the first-draft design. What matters the most now is the risk layer which is highly more concentrated and valuable than before: licensing, ledger accuracy, credit decisioning, and compliance audits.

The most effective approach is to consider a team that uses AI to complete 70% of the easy tasks so that the best engineers and specialists can use 30% that sink the business.

That is why a serious BNPL build costs what it costs. And it is precisely the part worth bringing an experienced partner in for.

What is the Cost to Build a BNPL App?

A BNPL platform is more than a simple mobile application. It can be considered a lending business with a checkout screen on top. Software development is often the fastest and most cost-effective part of the process. However, licensing, regulatory requirements, security audits, and banking relationships account for a significant share of the total investment, and these costs have not become any cheaper.

Therefore, there is no one-size-fits-all cost for BNPL app development. The total investment varies based on three factors: what it costs to build, what it costs to launch legally, and what it costs to operate. The figures also vary depending on the target market and licensing approach. Hence, treat them as directional ranges rather than fixed quotes.

| Cost layer | Lean (ride a licensed lender, single market) | Standard (hybrid license, GCC multi-market) | Enterprise (own license, multi-region, ML risk) | Does AI move it? |

|---|---|---|---|---|

| Engineering build (frontend, backend, core logic) | $40k–80k | $80k–150k | $150k–300k+ | Heavily. The biggest compression |

| UI/UX & product design | $10k–20k | $20k–40k | $40k–70k | Moderately |

| Licensing & regulatory setup (counsel, structuring, applications) | $15k–40k | $50k–150k | $150k–500k+ | Barely |

| Compliance & security (PCI-DSS, pen testing, AML setup, audits) | $20k–40k | $40k–90k | $90k–200k+ | Barely |

| Partnerships & integrations (sponsor bank, credit bureau, rails, KYC) | $10k–30k | $30k–80k | $80k–200k+ | Not at all. It is commercial |

| Ongoing ops & compliance (per year) | $40k–80k/yr | $80k–200k/yr | $200k–500k+/yr | Lightly |

The Build Is the Cheap Part. AI Made It Cheaper

The cost table reveals an essential pattern in BNPL app development. Engineering is no longer the largest cost component. AI has significantly improved development efficiency and reduced the time to build software. However, licensing, compliance, audits, banking partnerships, and ongoing operations account for a major share of the total investment.

A code generator does not shorten a license application, pass a PCI-DSS audit, or secure a sponsor bank relationship.

The old saying that “AI saves you 20%” is misleading. AI compresses the software development layer. However, the most consequential parts of launching and operating a BNPL business remain expensive and unchanged.

“AI makes it cheaper” is Only Half True

AI reduces much of the junior and repetitive work, allowing teams to deliver software faster with fewer resources. However, these savings are not free money. BNPL platforms still require senior fintech engineers who can architect critical systems such as double-entry ledgers, payment workflows, settlement mechanisms, and credit decisioning engines. As a result, teams become smaller and more specialized, but not automatically cheaper.

The Cost Not Reflected in the Table

One cost that is not showcased in the above table is lending capital, which is often the highest cost of running a BNPL platform. BNPL platforms provide funds to consumers and recover the payments over time.

A BNPL platform is generally a lender, and it requires a balance sheet or a warehouse facility to lend from. Based on the transaction volume and funding structure, the capital requirements often exceed the combined cost of development, compliance, and operations. That’s why a BNPL platform should be viewed more as a financial lending business and less as a software product.

How to Read the Tiers

The lean, standard, and enterprise tiers are not small, medium, and large applications. They indicate three unique regulatory and operational approaches.

A lean model operates in a single market with rules-based underwriting and is a cost-effective way to run a BNPL platform legally. Standard indicates a hybrid or own license across multiple GCC markets with ML-based credit scoring and risk assessment. An enterprise model holds a full license across multiple regions and manages end-to-end risk infrastructure internally. The increase in cost is often driven by compliance, operations, and capital requirements rather than features alone.

The Honest Takeaway: BNPL engineering is cheaper and faster than it has ever been. However, the total cost of launching and operating a compliant BNPL platform still remains higher than most guides admit. The most expensive components include licensing, compliance, partnerships, and lending capital, and these are areas that AI cannot significantly reduce.

Businesses that focus primarily on development costs often overlook the operational and regulatory commitments involved in running a BNPL platform. That’s where an experienced fintech partner adds the most value by helping businesses navigate the complexities that do not get cheaper over time.

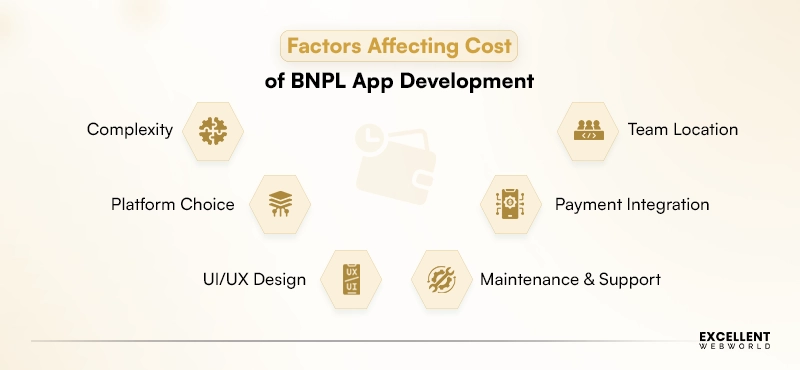

What are the Factors Affecting BNPL App Development Cost?

Some of the essential factors that affect Buy Now Pay Later app development cost include complexity, platform choice, UI/UX design, development team location, payment integration & security, and maintenance, which ultimately affect the budget and timeline.

What other Factors Affect the Cost of BNPL App Development?

The BNPL app development cost extends beyond the features and engineering effort. Factors such as the risk management, regulatory requirements, market expansion strategy, and operational infrastructure play a vital role in identifying the overall investment required to launch and scale a BNPL platform.

Risk and Money Movement

These factors directly affect the profitability and smooth financial operations of a BNPL platform by influencing risk management, cash flow, and repayment processes.

- Credit Decisioning Sophistication: Rule-based credit scoring is relatively affordable to implement. However, an advanced ML underwriting model requires data scientists, quality training data, continuous model monitoring, and ongoing optimization. The quality of the model directly affects default rates and overall P&L.

- The Fraud Stack: BNPL platforms are often prone to synthetic identities, account takeover, and first-party fraud. Consider integrating device fingerprinting, behavioral analytics, velocity checks, and third-party fraud detection systems. These increase the upfront and ongoing operational costs.

- Bureau and Alternative Data Costs: Every credit check includes per-request costs from credit bureaus. In thin-file GCC markets, where traditional data is limited, businesses often rely on alternative data sources, which can directly affect operational costs as transaction volume grows.

- Collections and Recovery Operations: Dunning flows, repayment restructuring, and late payment recovery are some of the common backend costs that most BNPL app budgets ignore. A BNPL platform without a structured collection strategy is one of the fastest ways to lose money.

- Settlement, Reconciliation, and Treasury Management: BNPL platforms must process, reconcile, and settle transactions across consumers, merchants, and banks. Treasury operations and daily reconciliation processes become increasingly complex and require significant resources as transaction volume grows.

Scope and Reach

The following factors determine the future-readiness, scalability, and adaptability of a BNPL platform across markets, merchants, and technologies.

- Number of Markets: Expanding into multiple countries increases licensing, compliance obligations, payment infrastructure, and operational needs. Each market introduces a new set of regulatory frameworks, which makes expansion a significant cost driver.

- Regional Localization: Localization extends beyond language support and translation. Every market introduces a new set of payment rails, such as KNET and Mada in the GCC, UPI in India, and SEPA in Europe. Each region has its own KYC norms, identity verification requirements, regulatory structures (for example, Sharia-compliant profit-fee models for Islamic markets), and data residency rules. All of these factors have an impact on development and operational costs.

- The Merchant Side is the Second Product: BNPL is B2B2C. Beyond the consumer app, businesses often require merchant onboarding systems, checkout integrations, SDKs, plugins, and merchant settlement workflows, which add another layer of development effort.

- AI-Native Scope: As AI-powered commerce grows, businesses are starting to invest in agent-consumable APIs, delegated consent frameworks, and agent verification mechanisms. Even though these capabilities are not mandatory, they help businesses reduce modernization costs and support emerging commerce experiences.

Build Choices

These decisions shape the overall cost structure by determining development approach, technology investments, team requirements, and platform scope.

- Build vs Buy: Using a BNPL or Banking-as-a-Service (BaaS) provider often reduces upfront development costs but introduces ongoing per-transaction fees. Developing core infrastructure internally often requires more investment but provides better control, flexibility, and higher margin potential.

- Enterprise Legacy Integration: Adding a BNPL platform into an existing retail or banking stack involves integrating with ERP systems, order management platforms, banking infrastructure, and payment ecosystems. This is often one of the most expensive aspects of an enterprise build and the area where AI provides the least support.

- Team Composition: AI has reduced repetitive development work, which enables teams to operate more efficiently. However, BNPL platforms still require highly experienced fintech engineers, architects, compliance specialists, and security experts. Hence, a small, experienced team can often deliver results comparable to a larger, lower-cost team.

- Platform Targets: Building for Android, iOS, and Web at the same time significantly increases development, testing, and maintenance costs compared to building for a single platform. Even though this is a straightforward decision for most BNPL products, the initial cost is real and should be included in the budget.

Ways to Reduce BNPL App Development Cost

Reducing BNPL app development cost is not just about lowering engineering expenses. Strategic decisions around licensing, infrastructure, market expansion, and risk management have a direct impact on the overall development cost.

Choose a Licensed Lending Partner: Partnering with a licensed lender or Banking-as-a-Service (BaaS) provider rather than holding your own license is cost-effective. It helps businesses save more costs than any code-level optimization.

Use a Managed Risk Architecture: Rather than building from scratch, businesses can leverage third-party services such as credit decisioning, fraud detection, KYC verification, and risk assessment from day one. Bring these in-house only when transaction volume justifies the cost of owning them.

Launch in One Market First: Expanding into multiple regions adds to the cost of licensing, compliance, and operations. Sequencing the launch allows businesses to reduce development cost and expand gradually while controlling expenses.

Phase the Underwriting: Businesses should introduce rules-based underwriting first. Add AI and ML-based credit scoring only when transaction volume is sufficient to justify the data science cost.

Do Not Cut Corners on Core Financial Systems: Cutting investment in ledger management, compliance, fraud detection, or security controls is one of the worst decisions any BNPL business can make. The cost of fixing them later far exceeds the cost of getting them right from the start.

Also Read: How to Reduce App Development Cost

Monetization & Revenue Model

A BNPL platform generates revenue via different methods to balance affordability with sustainable business growth. Let’s understand how BNPL apps make money and compare BNPL with traditional payment methods.

How BNPL Apps Make Money

BNPL apps generate revenue via merchant fees, user charges, interest on extended payments, and strategic partnerships to ensure sustainability with profitability.

| Monetization Models | Description |

|---|---|

| Merchant Fees | Merchants pay a specific fee, which is usually 2-8%, to the BNPL provider for every transaction on the platform. It covers charges of processing payments and offering BNPL services. |

| Late Fees | The BNPL platform charges late fees whenever a user misses a payment. This acts as a big source of revenue stream, urging timely payments and some sort of financial discipline. |

| Interest on Extended Payments | Consumers need to pay interest on the outstanding balance of the long-term payment plans, beyond short-term plans. Interest rates depend on the platform and region and help to generate predictive revenue for BNPL providers. |

| Subscription Fees | Launch a premium subscription plan with added benefits, such as high credit limits, lower interest rates, and exclusive merchant offers. This recurring revenue model offers a steady income beyond transaction-based earnings. |

| Data Monetization & Partnerships | BNPL platforms leverage user insights to form partnerships with merchants and financial institutions. These collaborations create value through targeted offers and shared revenue opportunities. |

BNPL vs Credit Card vs EMI

Here is how BNPL differs from traditional payment methods like Credit Cards and EMI across approval speed, interest structure, and repayment flexibility.

| Aspects | BNPL | Credit Card | EMI |

|---|---|---|---|

| Approval | Instant | Days to Weeks | Days to Weeks |

| Interest | Zero to Minimal | High Interest Rates | Moderate Interest Rates |

| Repayment | Fixed Short Installments (4to 6 Weeks) | Revolving Credit | Fixed Monthly Installments(3 to 24 Months) |

| Accessibility | High | Limited to Credit Users | Limited to eligible users |

| Use Case | Short-term purchases | Broad credit usage | High-value purchases |

| Late Fees | Fixed, transparent | Variable | Variable |

BNPL App Development Challenges and How to Overcome Them

Whenever building a BNPL App, there is a specific set of technical, financial, and regulatory issues that you might face. Here is a quick look at the key BNPL app development challenges along with their solutions.

1. Fraud and AI Arms Race

Challenge: BNPL platforms’ instant credit and digital onboarding make them a primary target for identity theft, synthetic identities, account takeover, and first-party fraud. Fraudsters have become more sophisticated and now use AI-generated identities and deepfakes, which makes standard rules-based checks ineffective.

Solution: Use a layered fraud detection strategy that combines device fingerprinting, behavioral analytics, transaction monitoring, and ML-based fraud detection. Most BNPL providers initially use managed fraud engines and progressively develop in-house capabilities as transaction volumes increase.

2. Credit Risk on Thin File Users

Challenge: Many BNPL users have little to no credit history, which makes traditional credit bureau scores less reliable. Poor credit assessment has a direct effect on profitability margin.

Solution: Use alternative data sources such as income patterns, utility payments, employment signals, and transaction behavior to feed ML models for informed credit decisions. Begin with rules-based underwriting and later consider data-science investment when data volume grows.

3. Maintaining Ledger Accuracy and Reconciliation

Challenge: This challenge is often overlooked and is a primary reason behind the failure of many BNPL platforms. Every transaction includes multiple parties, such as consumers, merchants, and sponsor banks, and the money must reconcile to the cent every day. Even a minor reconciliation error can result in settlement issues, accounting discrepancies, and compliance risks.

Solution: Build a double-entry immutable ledger as a single source of financial record from day one. Pair it with automated daily reconciliation and real-time tracking to identify and resolve discrepancies instantly.

4. Regulatory Compliance Across Markets

Challenge: BNPL regulations differ by market and are tightening fast. Affordability checks, disclosure rules, and licensing requirements evolve constantly across different regions, which makes multi-market compliance a significant operational challenge.

Solution: Engage regulatory experts at an early stage and design compliance as a configurable layer. This enables businesses to implement market-specific rules such as disclosures, affordability thresholds, and reporting formats without extensive redevelopment when regulations change.

5. Protecting Financial and Customer Data

Challenge: BNPL platforms store large volumes of personal and financial information, making them targets for cyberattacks and compliance obligations under GDPR, CPRA, PDPL, and DPDP. Each regulatory framework comes with different consent and data management requirements.

Solution: Implement encryption in transit and at rest, tokenization of payment and identity data, role-based access controls, and secure data storage practices. Businesses should enforce regional data residency requirements during architecture planning, not after deployment.

6. Managing Delinquencies and Collections

Challenge: Failed auto-debits due to expired cards or insufficient funds are one challenge, while genuine delinquencies are another. Without a structured collections strategy, a BNPL platform can lose significant revenue over time.

Solution: In the case of failed debits, consider automated payment retries, flexible repayment options, and timely alerts. For serious delinquencies, implement soft reminders, repayment restructuring, and formal collections in accordance with market-specific consumer protection regulations.

7. Merchant Integrations, Settlements, and Disputes

Challenge: Merchants operate on different technology stacks, which makes integration challenging. In addition, managing settlements, refunds, and disputes introduces further complexity. For instance, incorrect handling of a four-installment repayment plan can lead to reconciliation issues.

Solution: Develop an API-first architecture compatible with prebuilt SDKs and integrations for leading eCommerce platforms. Design settlement, refund, and dispute workflows early to ensure accurate installment adjustments and merchant payouts rather than treating them as an afterthought.

8. Ensuring Scalability During Peak Demand

Challenge: Seasonal sales, festive offers, and payday cycles can lead to significant transaction spikes. Performance issues during these periods can directly affect customer trust and increase declined transactions.

Solution: Implement a scalable microservices architecture with independent autoscaling for checkout, decisioning, and payment services. Regular load testing helps ensure the platform delivers consistent performance during peak demand periods.

9. Improving Consumer Transparency and Affordability

Challenge: Users often misunderstand repayment terms, which can lead to missed payments, regulatory scrutiny, and customer complaints. Therefore, clear disclosures and affordability checks are becoming mandatory in many markets.

Solution: Present repayment schedules, fees, and financing terms in simple, easy-to-understand language. Combine this with affordability checks at the point of sale and proactive payment reminders to improve customer trust.

10. Preparing for Agentic Commerce

Challenge: As AI agents begin transacting on users’ behalf, a new challenge emerges. Verifying whether an agent is acting with genuine, authorized consent when no human is present during the transaction introduces a new security and authorization risk.

Solution: Architect agent-consumable APIs, auditable consent mechanisms, and advanced verification frameworks to differentiate authorized AI agents from fraudulent activity. Building for this in advance protects the BNPL platform as agentic commerce continues to grow.

Future Trends in BNPL App Development

The latest innovations and evolving customer expectations, driven by emerging eCommerce trends, are shaping the future of BNPL. Here are the trends that will redefine the entire BNPL industry.

- Agentic commerce as a primary channel: AI agents can discover products, compare options, and complete purchases on behalf of consumers. As adoption grows, BNPL providers are embedding financing options directly into AI-driven purchase journeys to support seamless transactions.

- AI-native payments: Agent verification, real-time consent, and secure payment frameworks(Visa, Mastercard) are shaping the future of BNPL. These capabilities help platforms support autonomous transactions along with maintaining security, compliance, and user trust.

- Embedded Everywhere: BNPL is increasingly integrated into marketplaces, SaaS platforms, digital wallets, and super apps. As financing becomes part of the overall user journey, payments happen seamlessly in the background rather than as a separate checkout step, which leads to improved customer experiences and higher conversion rates. This shift is driving the adoption of AI agents to automate financing decisions and deliver more personalized payment experiences. As a result, many fintech businesses are looking to build AI agents that enable smarter and more personalized BNPL experiences.

- BNPL for B2B Payments: BNPL is now for B2B payments, which allows businesses to manage cash flow and offer deferred payment terms for high-ticket purchases & operational expenses.

- Omnichannel BNPL: BNPL now extends its availability for physical point-of-sale terminals for in-store and integrates with digital wallets in online stores.

- Convergence with Super Apps & Wallets: BNPL integration with Super Apps and digital wallets makes it a core tool for the financial ecosystem and enhances performance across financial services.

- Enhanced Security & Biometrics: With increasing online fraud, implementing biometric authentication and behavioral analytics is necessary for BNPL platforms to prevent risks and enhance users’ trust.

Can AI Alone Build a Successful BNPL App?

AI tools are constantly changing app development by improving productivity and accelerating delivery timeliness. However, building a successful BNPL app doesn’t just rely on generating code. As a fintech product, a BNPL solution operates in a highly regulated environment and must meet strict security, compliance, performance, and user trust requirements.

While AI can assist with coding, testing, documentation, and automation, businesses still need experienced BNPL technology partners to manage:

- Financial product and agent-interaction architecture

- Payment gateway, network, and agent-framework integrations

- KYC and AML workflows and scoped consent design

- Data security and multi-region compliance requirements

- Cloud infrastructure, scalability, and performance

- Scalability and performance optimization

- Long-term product strategy and support

Most successful BNPL applications combine the efficiency of AI-assisted development with the expertise of fintech developers, UI/UX designers, and product strategists. This approach enables businesses to accelerate innovation while ensuring long-term stability, compliance, scalability, and sustainable growth.

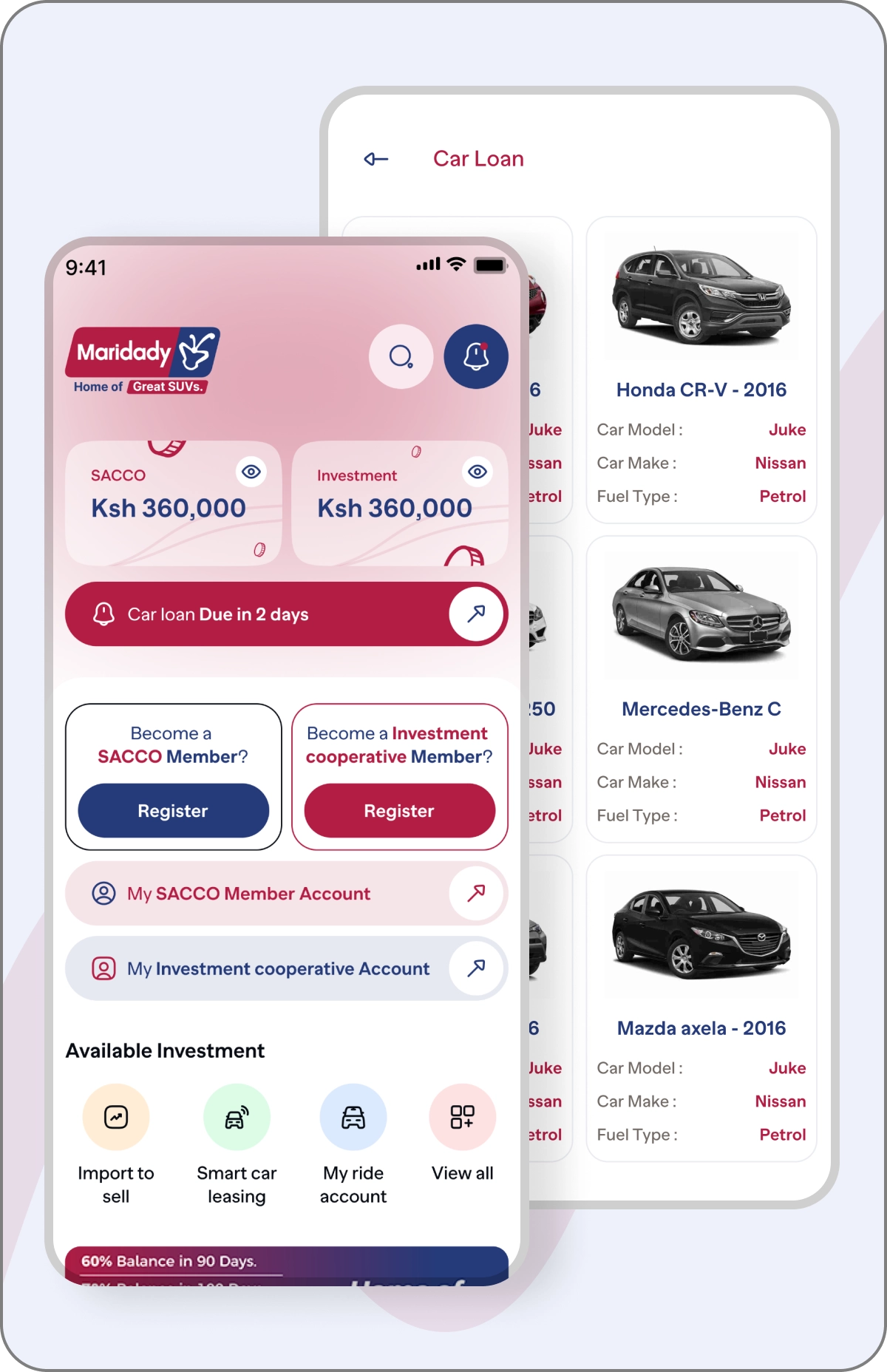

AI-Powered Automotive Finance Simplifies Multi-Model Vehicle Lending

We developed the Maridady Motors end-to-end financial platform to unify Kenya’s most fragmented car finance ecosystem into a unified lending and investment platform. It uses M-Pesa integration, CRB credit intelligence, and real-time portfolio management to turn transactional data into structured credit profiles, support five finance models, and contribute to a 38% higher approval rate.

- Supports asset finance, SACCO savings, hire purchase, lay-by, Flexi-Pay, and BNPL

- Tracks repayments, investments, and loan portfolios in real time

- Integrates M-Pesa and CRB for faster credit assessment

- Reduces underwriting time by 2.1x for loan officers

Wrapping up BNPL App Development Journey

BNPL app development is evolving faster than ever as AI-powered commerce, embedded finance, and agentic commerce continue to reshape how consumers discover, finance, and complete online purchases. Even though AI has accelerated research, design, development, and testing, the success or failure of a BNPL application still relies on strong financial infrastructure, compliance, risk management, and scalable architecture.

If you’re planning to build a future-ready BNPL solution, consider reaching out to the right technology partner. Excellent Webworld is an eCommerce app development company with AI engineers and fintech specialists. Our team implements the latest BNPL trends and uses AI-driven tools to help businesses architect secure, scalable, and agent-ready BNPL platforms that align with modern commerce experiences and long-term business growth.

FAQs on BNPL App Development

Agentic Commerce is the latest evolution of eCommerce where AI agents can discover products, compare options and prices, and complete entire purchases on a user’s behalf within defined limits. Rather than going through hundreds of websites, users can simply provide instructions to an AI agent and let it handle the purchasing process.

As these experiences become the new normal, BNPL providers need to ensure that their platforms can participate in AI-powered purchasing journeys through conversational and AI-driven checkout experiences. This requires modern capabilities, such as agent-consumable APIs, machine-readable financing offers, consent management, and agent verification mechanisms, to enable secure and compliant transactions.

AI definitely helps reduce the time needed for research, design, development, and testing. Despite this, licensing, compliance obligations, banking collaborations, risk management, and financial infrastructure remain the primary cost drivers that require human expertise and investment.

BNPL platforms operate in a regulated financial environment. Licensing requirements, KYC and AML obligations, security audits, regulatory reporting, and consumer protection rules often increase the total platform cost more than software development itself.

Agent-ready features allow BNPL platforms to communicate with AI shopping assistants and autonomous purchasing systems. These capabilities usually include agent-consumable APIs, machine-readable financing offers, agent verification, and auditable consent management.

Yes. As AI-powered commerce evolves, BNPL is becoming part of AI-assisted purchasing journeys rather than remaining a standalone checkout option. BNPL providers that invest in agent-ready infrastructure today will be better positioned to support future commerce experiences and deliver more seamless purchasing journeys for customers.

Buy Now, Pay Later (BNPL) Merchant Discount Rates (MDR) generally fall in the range of 2% to 8%, based on factors such as industry, order value, and provider policies. While the fee is higher than most traditional payment methods (such as credit/debit cards), many businesses offset the cost through increased conversions, reduced cart abandonment, and higher average order values.

In Buy Now, Pay Later transactions, the BNPL provider (such as Affirm, Klarna, etc.) bears the financial risk of credit underwriting, fraud prevention, and repayment collection. Merchants usually receive 100% payment upfront once the transaction is approved, while BNPL providers absorb the losses when a customer defaults or a bad actor makes unauthorized transactions.

Yes, businesses often observe a 40% to 70% increase in average order value after integrating BNPL and offering flexible payment options. It can also reduce cart abandonment and encourage higher-value purchases, making it a popular payment solution for eCommerce businesses.

Most leading BNPL providers offer detailed APIs, SDKs, and ready-made integrations for web, iOS, and Android platforms. The integration process is typically straightforward; however, businesses should also consider handling refunds, cancellations, payment status updates, and compliance requirements.

Regulations for BNPL are tightening globally. In the US, the CFPB classifies certain BNPL accounts under Regulation Z, while in India, the RBI mandates strict KYC and lending disclosure requirements. Therefore, BNPL providers and businesses must comply with regulations related to lending disclosures, consumer protection, KYC verification, data privacy, and affordability assessments before launch.

Article By

Paresh Sagar is the CEO of Excellent Webworld. He firmly believes in using technology to solve challenges. His dedication and attention to detail make him an expert in helping startups in different industries digitalize their businesses globally.